89bio: Pegozafermin Could Be A Game-Changer For Liver Disease – Strong Buy (NASDAQ:ETNB)

")

mi-viri

89bio, Inc. (NASDAQ:ETNB) is a clinical-stage biopharmaceutical company based in San Francisco, California. The company focuses on developing therapies for liver and cardiometabolic conditions with its drug candidate, pegozafermin. This medicine is a fibroblast growth factor 21 (FGF21) analog used to regulate metabolic processes like glucose and lipid metabolism. It is indicated for metabolic dysfunction-associated steatohepatitis [MASH] and severe hypertriglyceridemia [SHTG]. Pegozafermin has shown positive results in reducing liver fat and insulin resistance and alleviating liver fibrosis and inflammation. The drug is in phase 3 for MASH fibrosis, MASH cirrhosis, and SHTG.

Pegozafermin: Business Overview

89bio is a clinical-stage biopharmaceutical company founded in January 2018. It is based in San Francisco, California, and specializes in developing therapies for liver and cardiometabolic diseases. ETBN’s leading drug candidate is Pegozafermin, a fibroblast growth factor 21 [FGF21] analog, which means that it imitates the natural hormone FGF21 in its role in regulating metabolic processes like glucose and lipid metabolism to treat metabolic dysfunction-associated steatohepatitis [MASH] and severe hypertriglyceridemia [SHTG].

Source: 89bio, Inc. website.

MASH is a severe liver disease that presents symptoms that include inflammation and deterioration caused by excessive fat in the liver. SHTG involves high levels of triglycerides that can produce pancreatitis, cardiovascular disease, xanthomas, and hepatic steatosis, among several potential complications. Therefore, ETNB’s Pegozafermin is analogous to the FGF21 hormone that regulates metabolic-related processes. As a result, lipid oxidation increases, reducing lipogenesis and decreasing liver fat. The drug also improves insulin sensitivity and reduces liver inflammation and fibrosis. Hence, these action mechanisms should theoretically be effective treatments for MASH and SHTG.

Additionally, Pegozafermin uses glycoPEGylation technology with site mutations to prolong the half-life of the native FGF21 hormone. Thus, Pegozafermin helps balance liver-free fatty acid, improving its histology. Pegozafermin also increases the production of adiponectin, an insulin-sensitizing hormone with anti-inflammatory and anti-fibrotic properties. So overall, Pegozafermin is a promising compound as it acts across several mechanisms that holistically target causes of MASH, SHTG, and potentially other similar conditions.

Ongoing Trials and Updates

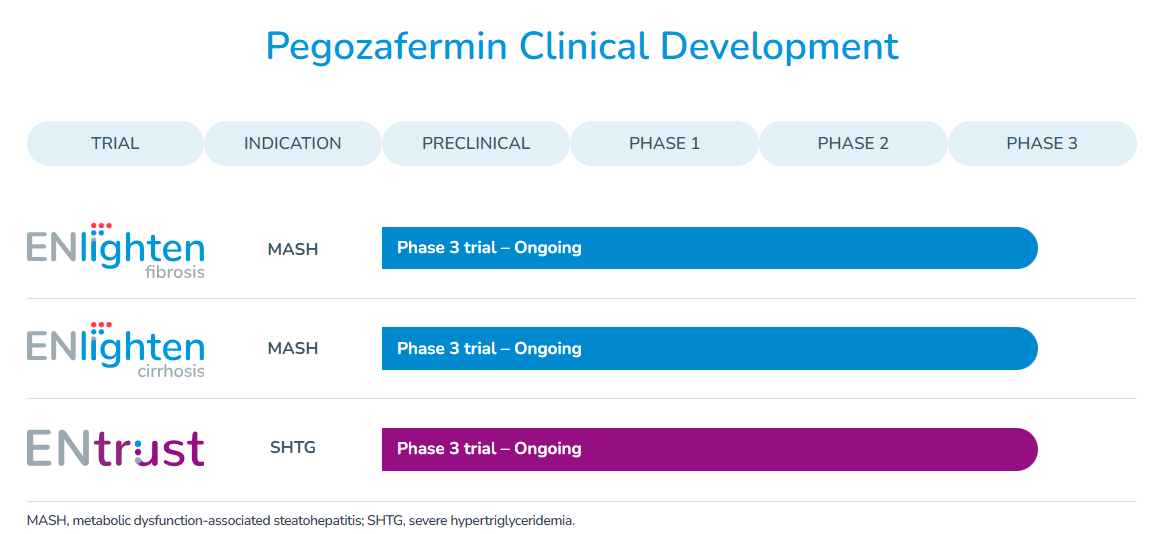

Currently, Pegozafermin is under three clinical trials in phase 3. The trial ENlighten studies fibrosis provoked by MAS. Another ENlighten trial evaluates the drug for cirrhosis due to MASH. The trial ENtrust for SHTG is also in phase 3. According to the company, MASH will impact around 27 million patients in the US by 2030 and a similar number in the EU. Plus, patients with fibrosis [F3 stage] and cirrhosis [F4 stage] are forecasted to reach 4.5 million and 3.1 million, respectively. This means that ETNB’s leading drug could potentially tap into a large market across different therapies, considering no current drug can cure MASH.

Moreover, ETNB estimates Pegozafermin will capture 23% market share in F2 MASH and 29% in F3 treatments, according to a survey conducted among hepatologists and gastroenterologists in September 2023. The drug can be prescribed as a monotherapy or in combination with GLP1 therapy. Plus, Pegozafermin was granted FDA Breakthrough Therapy designation for treating MASH with fibrosis. This is a relatively flexible compound that ETNB could research further to unlock additional FDA-approved indications, implying the potential for expanded revenue verticals if successful.

Source: Corporate Presentation. May 2024.

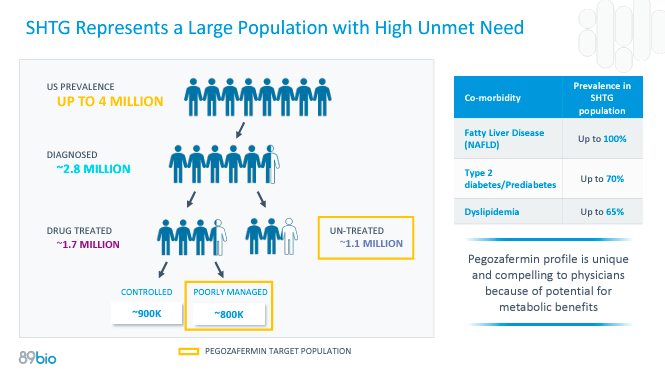

On the other hand, SHTG also has a substantial market, with a US patient prevalence of up to 4 million. Out of those 4 million, approximately 2.8 million patients are diagnosed, and around 1.7 million are treated, leaving at least 1.1 million remaining untreated. Hence, ETNB’s strategic focus is on severe metabolic conditions through a drug mimicking FGF21 hormone activity, which should theoretically go beyond just MASH and SHTG. If we look at it from first principles, Pegozafermin’s action mechanism could also be helpful for patients with Type 2 Diabetes Mellitus, Obesity, inflammatory diseases in general, and even cardiovascular indications in some circumstances. After all, the FGF21 hormone helps with insulin regulation, energy expenditure, and metabolism, reduces fat accumulation, and has anti-inflammatory properties.

PRIME Status and Partnership Potential

In March 2024, ETNB received Priority Medicines [PRIME] status from the European Medicines Agency [EMA] for its drug in treating MASH with fibrosis and cirrhosis. This designation was supported by the positive results obtained in the phase 2b ENliven trial conducted with 192 patients to evaluate safety and efficacy during 48 weeks with pegozafermin at 15 mg, 30 mg, and 44 mg versus placebo. The drug achieved statistical significance on primary endpoints, such as the proportion of the cohort with a resolution of MASH without worsening of fibrosis and the proportion of participants with ≥ 1 stage decrease in fibrosis stage with no worsening of MASH at week 24. Secondary endpoints were changes from baseline in liver fat, enzymes, markers of liver fibrosis, glycemic control, lipoproteins, and body weight. These measures were also positive indicators for the drug.

Source: Corporate Presentation. May 2024.

Then, in April 2024, 89bio partnered with Biopharma Engineering [BiBo], a Chinese company. BiBO will build a production facility in Shanghai’s pilot free trade zone for pegozafermin commercialization. ETNB will pay BiBo $135 million for the facility’s construction, and 45% will be payable in Q3 2024. The company believes this will provide enough manufacturing capacity to meet the drug’s large market requirements, suggesting that ETNB anticipates Pegozafermin will be a commercial success.

Promising at a Discount: Valuation Analysis

From a valuation perspective, ETNB is a moderately sized company, trading at a $880.5 million market cap. However, since it remains a pre-revenue company for now, the market is clearly pricing in some degree of success with Pegozafermin. For context, ETNB’s balance sheet holds $217.6 million in cash and $344.7 million in short-term investments, implying total liquidity as of Q1 2024 of $562.3 million. ETNB also has a negligible total debt of just $25.0 million, plus some operating lease obligations.

I also estimate that ETNB’s latest quarterly cash burn was just $39.7 million, which would be $158.8 million annually. Thus, this would imply that ETNB has a cash runway of roughly 3.5 years at this rate, which is relatively healthy as it gives the company ample room for maneuvering as needed.

Source: Corporate Presentation. May 2024.

Lastly, ETNB’s equity book value as of Q1 2024 was $510.5 million. This means it’s trading at a P/B ratio of 1.7, making it a self-evidently moderately priced stock. However, when we compare this valuation multiple to the sector’s median P/B ratio of 2.5, ETNB emerges as a promising biotech stock trading at a clear discount relative to its peers. When we also consider that ETNB is essentially at the late stages of its FDA approval process for Pegozafermin, it leads me to rate the stock as a “strong buy” at these levels for investors looking for exposure across several potential indications on metabolic-related diseases. Especially because I believe Pegozafermin’s indications could extend beyond just MASH and SHTG.

Investment Caveats: Risk Analysis

Naturally, the main risk is that even though ETNB’s IP is promising, it still doesn’t have the required FDA approvals for commercialization. Hence, new investors would be exposed to headline risk, and any meaningful setbacks or outright FDA rejections for Pegozafermin would quickly lead to price losses for shareholders. Even though it’s designated as a “Breakthrough Therapy,” this doesn’t guarantee FDA approval. There’s still the risk of Pegozafermin failing to prove its efficacy in larger phase 3 trials. And even if it’s effective, it might not be tolerable enough to satisfy the FDA’s approval requirements. So, investors must be aware of these risks before proceeding.

Moreover, market adoption isn’t guaranteed even if the drug is approved. In this piece, I’ve used ETNB’s market size estimates and their forecasted market share for when it’s launched. However, the reality is that several variables outside the company’s control will heavily influence its commercial success, such as insurance policies, pricing, and even healthcare provider idiosyncratic criteria. But despite these risks, I think that on the bigger picture, Pegozafermin does have a clear and reasonable path forward for eventual FDA approval and successful commercialization. ETNB’s balance sheet is robust, and management has enough room to maneuver if necessary, so dilution isn’t a concern for shareholders either. Hence, in my opinion, the risks are justified, and if ETNB is successful, it could unlock significant shareholder value through Pegozafermin in the long run.

Source: TradingView.

Strong Buy: Conclusion

Overall, ETNB is a compelling investment in biotech for investors seeking exposure to metabolic-related diseases. ETNB’s flagship drug candidate, Pegozafermin, is only in ongoing clinical trials for MASH and SHTG. However, I think its underlying action mechanisms could extend beyond these two indications into broader applications, potentially unlocking additional revenue verticals for ETNB. Moreover, the stock seems to be trading at a discount relative to its peers, and the price has pulled back significantly from its previous all-time highs. Hence, ETNB is a compelling “strong buy” at these levels despite the inherent biotech risks.

link

Is It Worth It?")